Every year, I have conversations with parents whose son or daughter has just committed (or spent their first year) at Texas A&M, and before long the housing question comes up.

“Should we buy something instead of renting?”

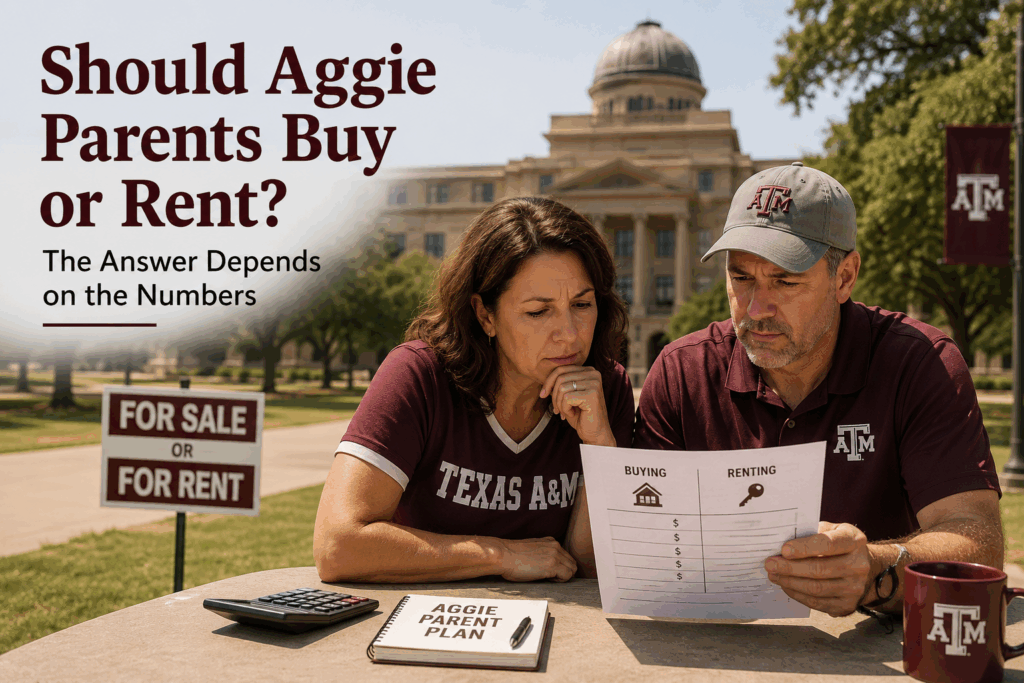

It’s a fair question. After all, if your student will be in Aggieland for four or five years, it’s natural to wonder whether all that rent money could go toward something you own instead. The reality is that sometimes buying makes a lot of sense.

And sometimes it doesn’t.

That’s probably not the answer most people expect from a REALTOR®, but it’s the truth. Over the years, I’ve worked with plenty of Aggie families who ultimately decided that renting was the better option for their situation. I’ve also worked with families who purchased a property, built equity over time, and walked away with a positive financial outcome when their student graduated.

The key is understanding the difference between the two before making a decision.

Looking Beyond the Monthly Payment

One of the biggest mistakes families make is comparing a mortgage payment to a rent payment and stopping there. Real estate is rarely that simple. When you purchase a property, you’re also taking on property taxes, insurance, maintenance, repairs, and transaction costs associated with eventually selling the home. At the same time, ownership creates opportunities that renting doesn’t. Part of your payment may build equity. The property may appreciate over time. Depending on the type of property, additional bedrooms may help offset ownership costs through rental income from roommates. That’s why every situation needs individual evaluation.

The question isn’t whether buying is better than renting.

The question is whether buying is better than renting for your family.

Generally speaking, ownership becomes more attractive when a student plans to remain in College Station for several years and the family has a longer-term outlook. Sometimes parents purchase a home, condo, or townhome knowing that younger siblings may eventually attend Texas A&M. Other times they intend to keep the property as a long-term investment after graduation. In those situations, building equity while providing housing can become part of a larger financial strategy. But even then, the numbers still matter. A property that looks good emotionally isn’t always a sound investment.

When Renting Is the Better Move

Plenty of situations exist where renting is the smartest decision. Maybe your student isn’t sure how long they’ll stay in College Station. Maybe you don’t want the responsibility of managing a property from another city. Maybe the available inventory doesn’t support your financial goals. And sometimes families simply value flexibility more than ownership. There’s nothing wrong with that. In fact, one of the best outcomes we can provide is helping someone avoid buying a property that doesn’t fit their objectives. At Bock Realty Group, we don’t start by asking whether you want to buy. We start by asking what you’re trying to accomplish. Once we understand your goals, we can run real numbers and compare the options side by side. We’ll look at the purchase price, financing, taxes, insurance, expected rents, projected holding periods, and potential exit strategies. Sometimes the analysis points toward ownership. Sometimes the analysis points toward renting. Either way, you’ll have a decision based on facts instead of assumptions.

Final Thoughts

The Bryan/College Station area is a unique market because of the constant demand generated by Texas A&M University. That creates opportunities for some families to turn a housing expense into a long-term asset. But opportunities and guarantees are not the same thing. The best decision aligns with your family’s goals, timeline, and financial situation. As both a REALTOR® and someone who believes strongly in making data-driven decisions, my advice is simple: don’t start with the assumption that buying is the answer. Start with the numbers. Sometimes those numbers support renting. Sometimes they support ownership. Our job at Bock Realty Group is to help you understand that difference.

This article is for general informational purposes only and is not legal, tax, or financial advice. Laws and programs can change, and individual circumstances vary. Consult qualified legal, tax, and lending professionals for advice specific to your situation.

Written by: Roy May Jr.